https://tysonspeaks.blogspot.com/2019/08/ifrs-16-sales-and-leaseback-part-1.html

Before you read this post, I would strongly recommend you to read Part 1 because Part 1 contains all the detailed explanations on the reasons behind the accounting for sales and leaseback.

For this post, I am going to focus on the scenarios in which the sales proceed received by the seller / lessee is not at fair value.

Basically, there are two possible scenarios, i.e.

1. The sales proceed received by seller is more than the fair value of the asset - to treat the additional proceed as additional financing.

|

| Why you can sell it at a more expensive price? Because the extra money you receive is a loan lah duh! You need to pay back the loan you know! Come on lah, the money is not free for you ok! |

2. The sales proceed received by seller is less than the fair value of the asset - to treat the difference between sales proceed and fair value as prepayment of lease payment.

|

| Aiyo, expensive also you ask, cheap also you ask, what you want lah? The reason why you sell it cheaper is because the buyer assume you already made a prepayment lah duh! You think you get free lunch in this world is it? |

Anyway enough with all these nonsense 😂😂😂. Let's get back to business.

We shall use the same illustration in Part 1, but with some minor modifications (the modification is shown as bold text).

Accounting for Seller / Lessee

Scenario 1 - Sales Proceed Received is Higher Than Fair Value

Company A sells a building to Company B for cash of $2 million. The fair value of the building is $1.8 million. The carrying amount of the building immediately before the sale is $1 million.

At the same time, Company A enters into a contract with Company B for the right to use the building for 18 years, with annual payments of $120,000 payable at the end of each year. The interest rate implicit in the lease is 4.5%, which results in a present value of the annual payments of $1,459,200.

The sale of the building to Company B meets the definition of a sale under IFRS 15.As noted in the bold sentence above, the sales proceed of $2 million is higher than the fair value of the building of $1.8 million. The additional $0.2 million will be treated as additional financing (i.e. additional loan from the lessor).

Let's follow through the four (4) steps required for seller / lessee.

Step 1 - Derecognise the Asset

The double entry for derecognition will be as follows:

Dr Bank $2 million

Cr PPE $1 million

Cr Lease liability (additional financing) $0.2 million

Cr Gain on disposal $0.8 million

As shown above, the gain on disposal of $0.8 million is calculated as the difference between the fair value of the asset ($1.8 million) and the carrying amount of the asset ($1 million). The additional financing of $0.2 million is recognised separately in the above entry.

Step 2 - Recognise the Leaseback

Dr Right-of-use Asset $1,259,200

Cr Lease liability $1,259,200

Take note that we only recognise $1,259,200 (not $1,459,200) in this step. This is because the present value of the annual payments of $1,459,200 also includes the additional financing of $200,000. As we have already recognised the additional financing of $200,000 in Step 1, we can only recognise $1,259,200 in Step 2 ($1,459,200 - $200,000). Otherwise the lease liability will be overstated.

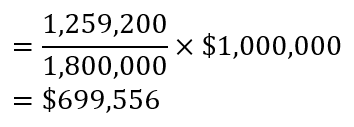

Step 3 - Calculate the Gain Attributable to Seller / Lessee (Gains Related to Portion Not Transferred to Buyer / Lessor)

Take note that as we have additional financing of $200,000, we need to remove it from the ratio calculation (as shown above). We can only compare $1,259,200 (the lease payment without additional financing) with the fair value of $1,800,000 (also without additional financing) so as to achieve apple with apple comparison.

|

| Apple with apple, perfectly balanced, as all things should be. |

| Yeah, yeah, Thanos, you are right. But can you please don't suddenly appear in my blog post and randomly share some life lessons? It is very annoying you know! 😂 |

Anyway, the gain attributable to seller / lessee will be as follows:

Step 4 - Remove the Gain Attributable to Seller / Lessee from Total Gain

Dr Gain on disposal $559,644

Cr Right-of-use asset $559,644

Summary

In summary, below represents the double entry for the sales and leaseback:

Dr Bank $2,000,000

Dr Right-of-use Asset (1,259,200-559,644) $699,556

Cr PPE $1,000,000

Cr Lease liability (200,000+1,259,200) $1,459,200

Cr Gain on disposal (800,000-559,644) $240,356

Alternatively, the right-of-use asset can also be calculated using the following method:

Right of use asset

= Ratio of portion attributable to seller or lessee x Previous carrying amount of the asset

Consistent with the logic of partial disposal, the right-of-use asset represents the portion of the previous carrying amount of the asset retained by the seller / lessee.

Scenario 2 - Sales Proceed Received is Lesser Than Fair Value

Company A sells a building to Company B for cash of $2 million. The fair value of the building is $2.2 million. The carrying amount of the building immediately before the sale is $1 million.

At the same time, Company A enters into a contract with Company B for the right to use the building for 18 years, with annual payments of $120,000 payable at the end of each year. The interest rate implicit in the lease is 4.5%, which results in a present value of the annual payments of $1,459,200.

The sale of the building to Company B meets the definition of a sale under IFRS 15.As noted in the bold sentence above, the sales proceed of $2 million is lower than the fair value of the building of $2.2 million. The difference of $0.2 million will be treated as prepayment of lease payment.

In other words, the sales proceed of $2 million can also be broken down into the following:

1. Company A receives the proceed of $2.2 million when sell the building.

2. Then Company A will pay $0.2 million to the seller / lessor as prepayment.

$2.2 million received minus $0.2 million paid, hence we get $2 million net proceed.

Let's follow through the four (4) steps required for seller / lessee.

Step 1 - Derecognise the Asset

The double entry for derecognition will be as follows:

Dr Bank $2 million

Dr Lease prepayment $0.2 million

Cr PPE $1 million

Cr Gain on disposal $1.2 million

As shown above, the gain on disposal of $1.2 million is calculated as the difference between the fair value of the asset ($2.2 million) and the carrying amount of the asset ($1 million). The difference of $0.2 million is recognised separately as a lease prepayment.

Step 2 - Recognise the Leaseback

Dr Right-of-use Asset $1,659,200

Cr Lease liability $1,459,200

Cr Lease prepayment $200,000

In step 2, when we recognise right-of-use asset, the prepayment of $200,000 will be reclassified to right-of-use asset. According to paragraph 24(b) of IFRS 16, it is mentioned that the cost of the right-of-use asset shall comprise any lease payments made at or before the commencement date (i.e. prepayment).

The lease liability will be recognised at $1,459,200 and right-of-use asset will be the total of $1,459,200 and $200,000.

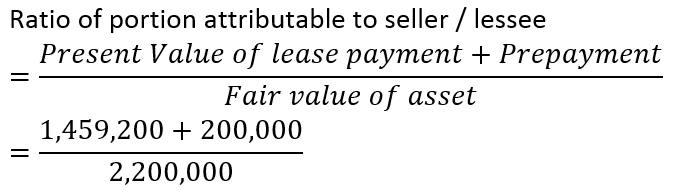

Step 3 - Calculate the Gain Attributable to Seller / Lessee (Gains Related to Portion Not Transferred to Buyer / Lessor)

Take note that as we have prepayment of $200,000, we need to include it into the ratio calculation (as shown above). We are comparing $1,659,200 (the lease payment together with prepayment) with the fair value of $2,200,000 (also includes prepayment) so as to achieve apple with apple comparison.

|

| Oops, I am sorry orange, even though both of you are fruits, an apple must still be compared with an apple, so I must politely say, "Please get out!" 😂😂😂 |

Anyway, the gain attributable to seller / lessee will be as follows:

Dr Gain on disposal $905,018

Cr Right-of-use asset $905,018

Summary

In summary, below represents the double entry for the sales and leaseback:

Dr Bank $2,000,000

Dr Right-of-use Asset (1,659,200-905,018) $754,182

Cr PPE $1,000,000

Cr Lease liability $1,459,200

Cr Gain on disposal (1,200,000-905,018) $294,982

Alternatively, the right-of-use asset can also be calculated using the following method:

Right of use asset

= Ratio of portion attributable to seller or lessee x Previous carrying amount of the asset

Consistent with the logic of partial disposal, the right-of-use asset represents the portion of the previous carrying amount of the asset retained by the seller / lessee.

Accounting for Buyer / Lessor (Relevant for SBR)

The accounting for buyer / lessor is the same as what I have explained previously in Part 1. You can refer to the explanation there.

Conclusion

Sales and leaseback can be complicated, but if we dissect the steps slowly and follow through the four steps that I have mentioned, I believe you will be able to understand them. As long as you understand the logic behind partial disposal, then you will be able to understand sales and leaseback. Wish you all the best in your studies and everything you do!

No comments:

Post a Comment