https://tysonspeaks.blogspot.com/2019/08/ias-12-how-to-determine-tax-base-part-1.html

In Part 1, we have covered the basic of deferred tax. In this post, we will cover the following:

1. Techniques that I use in determining tax base

2. Determining whether the temporary difference is taxable temporary difference (TTD) or deductible temporary difference (DTD).

For item no.1 above, the way that I use in determining tax base is by imagining the amount that would appear in the tax Statement of Financial Position (tax SOFP) if we prepare financial statements using tax rule.

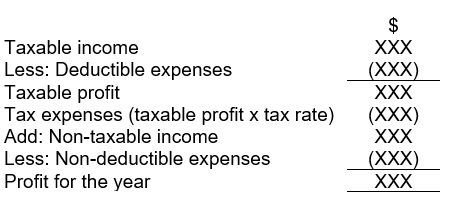

Tax Statement of Profit or Loss (Tax SOPL)

For tax purpose, we are concerned with taxable income and deductible expenses as these two items will determine taxable profit as well as the tax expenses. Thereafter, we also have the non-taxable income as well as non-deductible expenses in our tax SOPL. The final figure is the profit for the year.

Note: In practice we don't prepare SOPL using this manner. This is just my imagination.

Tax Statement of Financial Position (Tax SOFP)

If we prepare the SOPL using tax rule, the amount recognised in SOFP will also be different (due to different double entry).

The general idea is that tax base is the amount of asset or liability that is recognised in the tax SOFP if we prepare financial statements using tax rule.

Consider the definition of tax base in IAS 12 below:

The tax base of an asset or liability is the amount attributed to that asset or liability for tax purposes.We can thus interpret tax base as the amount that is recognised in tax SOFP.

In a tax SOFP, we also have asset, liability and equity. As we know the basic accounting equation is:

Asset - Liability = EquityIn any case, I came across the following in Facebook:

17 Equations that changed the World..

Posted by Electronic Engineering on Thursday, August 1, 2019

I was wondering why accounting equation is not included.

Allow me to add on the #18:

Accounting Equation: Asset - Liability = Equity

Luca Pacioli, 1494 😂😂😂

|

| Luca Pacioli, a.k.a. Thanos 😂😂😂 |

Anyway back to deferred tax. About the accounting equation, the idea when we calculate deferred tax is that we are going to compare all the assets and liabilities in both our accounting SOFP as well as tax SOFP (i.e. comparing carrying amount and tax base). We can ignore equity when we calculate deferred tax (since we already considered all the assets and liabilities).

Note: For this post, I will refer to the financial statements prepared using tax rule as "imaginary tax financial statements" because really, it is just my imagination ok 😂😂😂

You will understand more once you look into the different scenarios that I will illustrate below. But before we go into that, we will look into how do we determine whether a temporary difference is a taxable temporary difference or deductible temporary difference.

Taxable Temporary Difference (TTD) or Deductible Temporary Difference (DTD)?

In general, TTD means we are going to pay more tax in the future and DTD means we are going to pay lesser tax in the future. TTD will result in deferred tax liability whereas DTD will result in deferred tax asset. For the detailed explanation of what are these items, you can refer to Part 1.

There is a quick way to determine whether a temporary difference is TTD or DTD. You can use the following table in exam:

To illustrate:

1. For an asset, if the CA is larger than the TB, the difference is a TTD.

2. For an asset, if the CA is smaller than the TB, the difference is a DTD.

3. For a liability, if the CA is larger than the TB, the difference is a DTD.

4. For a liability, if the CA is smaller than the TB, the difference is a TTD.

All you need to do is to memorise the one that I highlighted in yellow (i.e. the first point above). For the rest, all you need to do is just to fill in the table by following the arrows as shown below:

When you fill in the table, all you need to do is to insert a reverse entry. In other words, for the column CA > TB, when you move down the arrow from TTD, you will fill in DTD. Then when you move to the right, you are going to fill in TTD. Then finally, when you move up, you will fill in DTD.

With this, we can now look into the different scenarios for deferred tax.

Tax Base of Assets

Before we go into the details, let's look at the definition of the tax base of an asset according to IAS 12:

(a) If an amount is deductible in the future (e.g. asset in which we can claim capital allowance), then that amount is the tax base for an asset.

(b) If we have an asset (e.g. receivable) in which we need not pay additional tax in the future when we receive the money, then tax base is equal to its carrying amount.

The various examples below would illustrate the two main points above.

1. Property, Plant and Equipment (PPE) which qualifies for capital allowance (tax depreciation)

This is the scenario that I have covered in Part 1. In this case, if we have a PPE in which we can claim capital allowance or tax depreciation, then we will have a tax base for that PPE.

Scenario: An entity purchased a machine for $100. The useful life is 5 years. For tax purpose, the entity can claim 50% tax depreciation. As such, for the first year,

CA = $100 - $100/5 = $80

TB = $100 - $100 x 50% = $50

If we were to apply tax rule in preparing financial statements, our tax SOFP will have an asset of $50 (after we charge 50% tax depreciation in our tax financial statements). As such, $50 is the tax base, indicating that we can claim $50 capital allowance in the future (an amount which is deductible in the future).

As we can see above, the CA is larger than TB. Referring to the table, as this is an asset, this represents a TTD which is equal to $30 ($80-$50).

Reason for TTD: The tax depreciation is faster than the accounting depreciation. In other words, the entity will pay lesser tax this year. In the future, the entity will have lesser or no tax depreciation if compared to accounting depreciation. This will result in higher tax payable in the future (hence TTD).

2. PPE which does not qualify for capital allowance (tax depreciation)

I have also covered this scenario in Part 1.

Scenario: An entity purchased a piece of land for $100 which does not qualify for capital allowance or tax depreciation.

If we were to prepare financial statements using tax rule, our imaginary tax double entry will be as follows (Note: this is not the real double entry. This is just my imagination of the double entry in the imaginary tax financial statements):

Dr Non-deductible expenses (Tax SOPL) $100

Cr Bank $100

In other words, since the land does not qualify for capital allowance, there is no asset in the tax SOFP. Therefore, the tax base of this land is zero because there is no amount of asset that will be deductible in the future.

As such, CA of the land is $100 and the TB is zero. This is the case when CA > TB. As this is an asset, the difference should be a TTD of $100 (but this is not true, read below).

In Part 1, I mentioned that no deferred tax is recognised for permanent difference. In this case, the difference is a permanent difference because the land will never be deductible for tax purposes (i.e. the accounting treatment will be forever different from the tax treatment). As such, we DO NOT calculate deferred tax for this scenario.

3. PPE under Revaluation Model (IAS 16)

Scenario: An entity purchased a piece of land for $100 which does not qualify for capital allowance or tax depreciation. The land is not depreciated for accounting purpose. However, the entity adopts revaluation model for land under IAS 16. As at year end, the fair value of the land has increased to $120.

Tax treatment: Assume that the land does not qualify for capital allowance. As such, the TB is zero. However, if the entity sell off the land in the future, the gain on disposal is taxable under capital gain tax (in Malaysia this is known as Real Property Gains Tax).

In this case, as explained above, the difference between CA and TB is permanent difference because the land does not qualify for capital allowance. As such, deferred tax calculation is not required.

However, deferred tax calculation will be required on the gain on revaluation as the entity will need to pay capital gain tax in the future. As the entity may need to pay extra tax in the future, this represents TTD and the TTD will be equal to the revaluation gain of $20 ($120-$100).

The accounting double entry for gain on revaluation is as follows:

Dr Land $20

Cr Other Comprehensive Income (OCI) / Revaluation Surplus $20

Notice that the gain is recognised in OCI under revaluation model. As such, it should be noted that the deferred tax on the gain on revaluation should also be recognised in the OCI (the deferred tax treatment should follow the accounting treatment of the asset).

Assuming a tax rate of 25%, the deferred tax liability will be equal to $5 ($20 x 25%). The accounting double entry for this deferred tax liability is:

Dr OCI / Revaluation Surplus $5

Cr Deferred tax liability $5

Take note of the highlighted debit entry, it is to OCI, not to Profit or Loss.

Refer to the following for the extract of the SOPL:

As you can see from the above, the debit entry of the deferred tax is recognised is recognised in OCI (not profit or loss). You can choose to show the deferred tax as a separate line in the OCI or to show the gain on revaluation net of tax (as shown in the extract above).

Note: If the land is an investment property under IAS 40 and it is held under fair value model (i.e. the change in fair value is recognised in SOPL), then the deferred tax will also be recognised in the SOPL. Again, the deferred tax treatment should follow the accounting treatment of the asset.

4. Development Cost (IAS 38)

:max_bytes(150000):strip_icc()/research_pharma-5bfc322b46e0fb0051bf11a0.jpg)

An entity incurs development cost of $100 and the entire $100 meets the criteria for capitalisation under IAS 38 Intangible Asset.

Tax treatment: Assume that development cost is deductible when it is incurred.

In this case, because the entity has incurred the development cost, the entity will be able to claim a tax deduction this year. The imaginary tax double entry for the imaginary tax financial statements shall be as follows:

Dr Deductible expenses $100

Cr Bank $100

In other words, since the entity has already claimed a deduction for development cost in the current year, there will be no asset in the tax SOFP (because there is no more deduction available in the future). Hence, the tax base is zero.

Therefore, CA = 100 and TB = 0 and as this is an asset, the difference of $100 will be TTD.

Reason for TTD: As the entity has already claimed deduction in this year, the entity will pay lesser tax this year. However, as the entity will have no more deduction in the future. the entity is going to pay more tax in the future. Hence, this is a TTD.

5. Inventory Written Down to Net Realisable Value (NRV)

Purchases of Inventory

When an entity purchases inventory for $100, they will include the inventory in their current asset by

Dr Inventory $100

Cr Bank $100

As such, the carrying amount of inventory is $100.

When the inventory is sold in the future, the entity will:

Dr Cost of sales $100

Cr Inventory $100

Tax treatment: Assuming that when the entity makes a purchase of inventory, a deduction cannot be given now. However, a deduction can be given when the inventory is sold in the future.

As such, the imaginary tax double entry that we have when we prepare the imaginary tax financial statements when we purchase inventory are as follows:

Dr Inventory $100

Cr Bank $100

In this case, we have a tax base of $100 because we can claim a deduction in the future when the inventory is sold.

When the inventory is sold in the future, the imaginary tax double entry will be:

Dr Deductible expenses $100

Cr Bank $100

As the CA = $100 and TB = $100 when the entity purchases the inventory, there will be no temporary difference and no deferred tax. This is because the accounting rule and tax rule are the same (as we can see, the accounting double entry and tax double entry is similar).

Write Down of Inventory

An entity purchased inventory for $100. The tax rule on purchase of inventory is similar to the previous illustration (i.e. deductible when inventory is sold in the future).

According to IAS 2, if the NRV of the inventory drop to $80 (e.g. due to damaged goods), by applying the lower of cost and NRV rule, the entity will write down the inventory to its NRV by:

Dr Cost of sales (SOPL) $20

Cr Inventory $20

As such, the carrying amount of the inventory is $80 ($100 - $20).

Tax treatment: Assuming that the write down of inventory is a non-allowable expense. However, such write down will only be permitted when the inventory is sold in future.

Because of the write down of inventory is not allowable in the current year, accordingly there is no tax double entry in the imaginary tax financial statements. The tax base of the inventory will remain at $100 as there is no adjustment for tax purpose.

In this case, the CA = $80 and TB = $100. As this is an asset and CA < TB, there will be a DTD of $20.

Reason for DTD: The entity cannot claim deduction for write down of NRV now. As such, the tax will be higher this year. In the future, when the inventory is sold, the entity can pay lesser tax as deduction will be given by then (hence DTD).

6. Impairment of Trade Receivables

Recognise Credit Sales

When an entity makes a credit sales of $100, the accounting double entry is:

Dr Trade receivables $100

Cr Revenue $100

The carrying amount of the asset (trade receivables) is $100.

Tax treatment: Assuming that credit sales is taxable even though the entity has not received the money from customer.

As such, the tax double entry in the imaginary tax financial statements will be similar to accounting double entry:

Dr Trade receivables $100

Cr Taxable income $100

The tax base of the asset (trade receivables) is $100.

In this case, as the CA = $100 and TB = $100, there will be no temporary difference and no deferred tax. This is because the accounting rule and tax rule are the same.

Impairment of Trade Receivables

Impairment of trade receivables is covered under IFRS 9 Financial Instrument. For example, if we have trade receivables of $100 and we have determined that the trade receivables has been impaired by $20, the accounting double entry is:

Dr Impairment of Trade Receivables (SOPL) $20

Cr Allowance for Impairment of Trade Receivables $20

The carrying amount of the trade receivables is $80 ($100 - $80).

Tax treatment: Similar to the previous illustration, credit sales of $100 is taxable. However, assume that impairment of trade receivables is not an allowable expense. Deduction can only be given in the future if the entity confirms that the trade receivables has already gone bankrupt.

Because of the impairment of trade receivables is not allowable in the current year, accordingly there is no tax double entry in the imaginary tax financial statements. The tax base of the trade receivables will remain at $100 as there is no adjustment for tax purpose.

In this case, the CA = $80 and TB = $100. As this is an asset and CA < TB, there will be a DTD of $20.

Reason for DTD: The entity cannot claim deduction for impairment of trade receivables now. As such, the tax will be higher this year. If the trade receivables really become bankrupt in the future, the entity will be able pay lesser tax in the future (hence DTD) when deduction for impairment of trade receivables is given.

7. Prepaid Expenses

An entity made an advance payment for electricity expenses for the next financial year (prepaid expenses) amounting to $100. The double entry will be:

Dr Prepaid expenses $100

Cr Bank $100

As such, carrying amount of the asset (prepaid expenses) is $100.

Tax treatment: Assuming that the tax law mentions that an entity can only make a deduction for an expense if the expense is paid (i.e. deduction is on cash basis)

In this case, as the entity has already made the payment of $100, the entity will be able to claim a deduction. The imaginary tax double entry in the imaginary tax financial statements will be as follows:

Dr Deductible expenses $100

Cr Bank $100

In other words, since the entity has already claimed a deduction for electricity expenses in this year, there will no asset in the tax SOFP because there is no more deduction available in the future. As such, the tax base is zero.

Therefore, CA = 100 and TB = 0 and as this is an asset, the difference of $100 will be TTD.

Reason for TTD: As the entity has already claimed deduction in this year, the entity will pay lesser tax this year. However, the entity will have no more deduction in the future. This will result in the entity to pay more tax (in relation to its accounting profit) in the future. Hence, this is a TTD.

Exam shortcut: This scenario is similar to development cost as explained above (the fourth scenario). Just remember that if the tax treatment provides that deduction is on a cash basis, then tax base will be equal to zero.

8. Income Receivable Which Is Taxed on Cash / Receipt Basis

An entity recognises interest income of $100 on accrual basis even though the entity has not received the interest income. The accounting double entry is:

Dr Interest receivable $100

Cr Interest income (SOPL) $100

As such, the carrying amount of interest receivable (asset) is $100.

Tax treatment: Assuming that the tax law mentions that interest income is only taxed when the entity receives the income (i.e. taxed on receipt or cash basis).

As the entity have not receive the income this year, the entity need not pay any tax on the interest income. Accordingly, the entity will not have any imaginary tax double entry.

In other words, because the interest income is not taxable this year, there will be no asset in the tax SOFP. The tax base of the asset will be zero.

Therefore, CA = $100 and TB = $0. As interest receivable is an asset, this represents TTD of $100.

Reason for TTD: The entity will not pay tax this year. However, the entity will pay more tax in the future when they receive the interest income. As such, it is a TTD.

Exam shortcut: As the tax treatment provides that the income will be taxed on receipt or cash basis, the tax base will be equal to zero.

9. Receivables for Non-Taxable Income

An entity has a dividend receivables of $100. The accounting double entry is

Dr Dividend receivables $100

Cr Dividend income $100

As such, carrying amount of the asset is $100.

Tax treatment: Assuming that dividend income is a non-taxable income.

The imaginary tax double entry in the imaginary tax financial statement is

Dr Dividend receivables $100

Cr Non-taxable income $100

Tax base is also equal to $100.

As the CA and TB are the same, there will be no deferred tax.

Note: As mentioned previously in the definition of tax base for asset, "if those economic benefits will not be taxable, the tax base of the asset is equal to its carrying amount."As dividend income is not taxable, the TB shall be equal to its CA.

Alternatively, you can also argue that as the income is not taxable, the difference represents a permanent difference and deferred tax should be ignored. Both analysis will result in no deferred tax calculation.

10. Loan Receivable

A loan receivable has a carrying amount of $100. The accounting double entry is:

Dr Loan Receivable $100

Cr Bank $100

As such, carrying amount of the asset is $100.

Tax treatment: When loan is given out, there is no tax consequence. When the loan is being repaid back to the entity, there is also no tax consequence.

In this case, the imaginary tax double entry in the imaginary tax financial statement is the same as the accounting double entry, i.e.

Dr Loan Receivable $100

Cr Bank $100

Tax base is also equal to $100.

As the CA and TB are the same, there will be no deferred tax.

Note: As mentioned previously in the definition of tax base for asset, "if those economic benefits will not be taxable, the tax base of the asset is equal to its carrying amount." As the repayment of loan has no tax implication (i.e.not taxable), the TB shall be equal to the CA.

That's all for this post! I believe you will have a lot to digest for now.

In my next post, I will discuss about how do we determine tax base for liability. Stay tuned!

With this, we can now look into the different scenarios for deferred tax.

Tax Base of Assets

Before we go into the details, let's look at the definition of the tax base of an asset according to IAS 12:

The tax base of an asset is the amount that will be deductible for tax purposes against any taxable economic benefits that will flow to an entity when it recovers the carrying amount of the asset. If those economic benefits will not be taxable, the tax base of the asset is equal to its carrying amount.In short, there are two main points:

(a) If an amount is deductible in the future (e.g. asset in which we can claim capital allowance), then that amount is the tax base for an asset.

(b) If we have an asset (e.g. receivable) in which we need not pay additional tax in the future when we receive the money, then tax base is equal to its carrying amount.

The various examples below would illustrate the two main points above.

1. Property, Plant and Equipment (PPE) which qualifies for capital allowance (tax depreciation)

This is the scenario that I have covered in Part 1. In this case, if we have a PPE in which we can claim capital allowance or tax depreciation, then we will have a tax base for that PPE.

Scenario: An entity purchased a machine for $100. The useful life is 5 years. For tax purpose, the entity can claim 50% tax depreciation. As such, for the first year,

CA = $100 - $100/5 = $80

TB = $100 - $100 x 50% = $50

If we were to apply tax rule in preparing financial statements, our tax SOFP will have an asset of $50 (after we charge 50% tax depreciation in our tax financial statements). As such, $50 is the tax base, indicating that we can claim $50 capital allowance in the future (an amount which is deductible in the future).

As we can see above, the CA is larger than TB. Referring to the table, as this is an asset, this represents a TTD which is equal to $30 ($80-$50).

Reason for TTD: The tax depreciation is faster than the accounting depreciation. In other words, the entity will pay lesser tax this year. In the future, the entity will have lesser or no tax depreciation if compared to accounting depreciation. This will result in higher tax payable in the future (hence TTD).

2. PPE which does not qualify for capital allowance (tax depreciation)

I have also covered this scenario in Part 1.

Scenario: An entity purchased a piece of land for $100 which does not qualify for capital allowance or tax depreciation.

If we were to prepare financial statements using tax rule, our imaginary tax double entry will be as follows (Note: this is not the real double entry. This is just my imagination of the double entry in the imaginary tax financial statements):

Dr Non-deductible expenses (Tax SOPL) $100

Cr Bank $100

In other words, since the land does not qualify for capital allowance, there is no asset in the tax SOFP. Therefore, the tax base of this land is zero because there is no amount of asset that will be deductible in the future.

As such, CA of the land is $100 and the TB is zero. This is the case when CA > TB. As this is an asset, the difference should be a TTD of $100 (but this is not true, read below).

In Part 1, I mentioned that no deferred tax is recognised for permanent difference. In this case, the difference is a permanent difference because the land will never be deductible for tax purposes (i.e. the accounting treatment will be forever different from the tax treatment). As such, we DO NOT calculate deferred tax for this scenario.

3. PPE under Revaluation Model (IAS 16)

Scenario: An entity purchased a piece of land for $100 which does not qualify for capital allowance or tax depreciation. The land is not depreciated for accounting purpose. However, the entity adopts revaluation model for land under IAS 16. As at year end, the fair value of the land has increased to $120.

Tax treatment: Assume that the land does not qualify for capital allowance. As such, the TB is zero. However, if the entity sell off the land in the future, the gain on disposal is taxable under capital gain tax (in Malaysia this is known as Real Property Gains Tax).

In this case, as explained above, the difference between CA and TB is permanent difference because the land does not qualify for capital allowance. As such, deferred tax calculation is not required.

However, deferred tax calculation will be required on the gain on revaluation as the entity will need to pay capital gain tax in the future. As the entity may need to pay extra tax in the future, this represents TTD and the TTD will be equal to the revaluation gain of $20 ($120-$100).

The accounting double entry for gain on revaluation is as follows:

Dr Land $20

Cr Other Comprehensive Income (OCI) / Revaluation Surplus $20

Notice that the gain is recognised in OCI under revaluation model. As such, it should be noted that the deferred tax on the gain on revaluation should also be recognised in the OCI (the deferred tax treatment should follow the accounting treatment of the asset).

Assuming a tax rate of 25%, the deferred tax liability will be equal to $5 ($20 x 25%). The accounting double entry for this deferred tax liability is:

Dr OCI / Revaluation Surplus $5

Cr Deferred tax liability $5

Take note of the highlighted debit entry, it is to OCI, not to Profit or Loss.

Refer to the following for the extract of the SOPL:

As you can see from the above, the debit entry of the deferred tax is recognised is recognised in OCI (not profit or loss). You can choose to show the deferred tax as a separate line in the OCI or to show the gain on revaluation net of tax (as shown in the extract above).

Note: If the land is an investment property under IAS 40 and it is held under fair value model (i.e. the change in fair value is recognised in SOPL), then the deferred tax will also be recognised in the SOPL. Again, the deferred tax treatment should follow the accounting treatment of the asset.

4. Development Cost (IAS 38)

An entity incurs development cost of $100 and the entire $100 meets the criteria for capitalisation under IAS 38 Intangible Asset.

Tax treatment: Assume that development cost is deductible when it is incurred.

In this case, because the entity has incurred the development cost, the entity will be able to claim a tax deduction this year. The imaginary tax double entry for the imaginary tax financial statements shall be as follows:

Dr Deductible expenses $100

Cr Bank $100

In other words, since the entity has already claimed a deduction for development cost in the current year, there will be no asset in the tax SOFP (because there is no more deduction available in the future). Hence, the tax base is zero.

Therefore, CA = 100 and TB = 0 and as this is an asset, the difference of $100 will be TTD.

Reason for TTD: As the entity has already claimed deduction in this year, the entity will pay lesser tax this year. However, as the entity will have no more deduction in the future. the entity is going to pay more tax in the future. Hence, this is a TTD.

5. Inventory Written Down to Net Realisable Value (NRV)

Purchases of Inventory

When an entity purchases inventory for $100, they will include the inventory in their current asset by

Dr Inventory $100

Cr Bank $100

As such, the carrying amount of inventory is $100.

When the inventory is sold in the future, the entity will:

Dr Cost of sales $100

Cr Inventory $100

Tax treatment: Assuming that when the entity makes a purchase of inventory, a deduction cannot be given now. However, a deduction can be given when the inventory is sold in the future.

As such, the imaginary tax double entry that we have when we prepare the imaginary tax financial statements when we purchase inventory are as follows:

Dr Inventory $100

Cr Bank $100

In this case, we have a tax base of $100 because we can claim a deduction in the future when the inventory is sold.

When the inventory is sold in the future, the imaginary tax double entry will be:

Dr Deductible expenses $100

Cr Bank $100

As the CA = $100 and TB = $100 when the entity purchases the inventory, there will be no temporary difference and no deferred tax. This is because the accounting rule and tax rule are the same (as we can see, the accounting double entry and tax double entry is similar).

Write Down of Inventory

|

| Damaged goods |

An entity purchased inventory for $100. The tax rule on purchase of inventory is similar to the previous illustration (i.e. deductible when inventory is sold in the future).

According to IAS 2, if the NRV of the inventory drop to $80 (e.g. due to damaged goods), by applying the lower of cost and NRV rule, the entity will write down the inventory to its NRV by:

Dr Cost of sales (SOPL) $20

Cr Inventory $20

As such, the carrying amount of the inventory is $80 ($100 - $20).

Tax treatment: Assuming that the write down of inventory is a non-allowable expense. However, such write down will only be permitted when the inventory is sold in future.

Because of the write down of inventory is not allowable in the current year, accordingly there is no tax double entry in the imaginary tax financial statements. The tax base of the inventory will remain at $100 as there is no adjustment for tax purpose.

In this case, the CA = $80 and TB = $100. As this is an asset and CA < TB, there will be a DTD of $20.

Reason for DTD: The entity cannot claim deduction for write down of NRV now. As such, the tax will be higher this year. In the future, when the inventory is sold, the entity can pay lesser tax as deduction will be given by then (hence DTD).

6. Impairment of Trade Receivables

Recognise Credit Sales

When an entity makes a credit sales of $100, the accounting double entry is:

Dr Trade receivables $100

Cr Revenue $100

The carrying amount of the asset (trade receivables) is $100.

Tax treatment: Assuming that credit sales is taxable even though the entity has not received the money from customer.

As such, the tax double entry in the imaginary tax financial statements will be similar to accounting double entry:

Dr Trade receivables $100

Cr Taxable income $100

The tax base of the asset (trade receivables) is $100.

In this case, as the CA = $100 and TB = $100, there will be no temporary difference and no deferred tax. This is because the accounting rule and tax rule are the same.

Impairment of Trade Receivables

Impairment of trade receivables is covered under IFRS 9 Financial Instrument. For example, if we have trade receivables of $100 and we have determined that the trade receivables has been impaired by $20, the accounting double entry is:

Dr Impairment of Trade Receivables (SOPL) $20

Cr Allowance for Impairment of Trade Receivables $20

The carrying amount of the trade receivables is $80 ($100 - $80).

Tax treatment: Similar to the previous illustration, credit sales of $100 is taxable. However, assume that impairment of trade receivables is not an allowable expense. Deduction can only be given in the future if the entity confirms that the trade receivables has already gone bankrupt.

Because of the impairment of trade receivables is not allowable in the current year, accordingly there is no tax double entry in the imaginary tax financial statements. The tax base of the trade receivables will remain at $100 as there is no adjustment for tax purpose.

In this case, the CA = $80 and TB = $100. As this is an asset and CA < TB, there will be a DTD of $20.

Reason for DTD: The entity cannot claim deduction for impairment of trade receivables now. As such, the tax will be higher this year. If the trade receivables really become bankrupt in the future, the entity will be able pay lesser tax in the future (hence DTD) when deduction for impairment of trade receivables is given.

7. Prepaid Expenses

An entity made an advance payment for electricity expenses for the next financial year (prepaid expenses) amounting to $100. The double entry will be:

Dr Prepaid expenses $100

Cr Bank $100

As such, carrying amount of the asset (prepaid expenses) is $100.

Tax treatment: Assuming that the tax law mentions that an entity can only make a deduction for an expense if the expense is paid (i.e. deduction is on cash basis)

In this case, as the entity has already made the payment of $100, the entity will be able to claim a deduction. The imaginary tax double entry in the imaginary tax financial statements will be as follows:

Dr Deductible expenses $100

Cr Bank $100

In other words, since the entity has already claimed a deduction for electricity expenses in this year, there will no asset in the tax SOFP because there is no more deduction available in the future. As such, the tax base is zero.

Therefore, CA = 100 and TB = 0 and as this is an asset, the difference of $100 will be TTD.

Reason for TTD: As the entity has already claimed deduction in this year, the entity will pay lesser tax this year. However, the entity will have no more deduction in the future. This will result in the entity to pay more tax (in relation to its accounting profit) in the future. Hence, this is a TTD.

Exam shortcut: This scenario is similar to development cost as explained above (the fourth scenario). Just remember that if the tax treatment provides that deduction is on a cash basis, then tax base will be equal to zero.

8. Income Receivable Which Is Taxed on Cash / Receipt Basis

An entity recognises interest income of $100 on accrual basis even though the entity has not received the interest income. The accounting double entry is:

Dr Interest receivable $100

Cr Interest income (SOPL) $100

As such, the carrying amount of interest receivable (asset) is $100.

Tax treatment: Assuming that the tax law mentions that interest income is only taxed when the entity receives the income (i.e. taxed on receipt or cash basis).

As the entity have not receive the income this year, the entity need not pay any tax on the interest income. Accordingly, the entity will not have any imaginary tax double entry.

In other words, because the interest income is not taxable this year, there will be no asset in the tax SOFP. The tax base of the asset will be zero.

Therefore, CA = $100 and TB = $0. As interest receivable is an asset, this represents TTD of $100.

Reason for TTD: The entity will not pay tax this year. However, the entity will pay more tax in the future when they receive the interest income. As such, it is a TTD.

Exam shortcut: As the tax treatment provides that the income will be taxed on receipt or cash basis, the tax base will be equal to zero.

9. Receivables for Non-Taxable Income

An entity has a dividend receivables of $100. The accounting double entry is

Dr Dividend receivables $100

Cr Dividend income $100

As such, carrying amount of the asset is $100.

Tax treatment: Assuming that dividend income is a non-taxable income.

The imaginary tax double entry in the imaginary tax financial statement is

Dr Dividend receivables $100

Cr Non-taxable income $100

Tax base is also equal to $100.

As the CA and TB are the same, there will be no deferred tax.

Note: As mentioned previously in the definition of tax base for asset, "if those economic benefits will not be taxable, the tax base of the asset is equal to its carrying amount."As dividend income is not taxable, the TB shall be equal to its CA.

Alternatively, you can also argue that as the income is not taxable, the difference represents a permanent difference and deferred tax should be ignored. Both analysis will result in no deferred tax calculation.

10. Loan Receivable

A loan receivable has a carrying amount of $100. The accounting double entry is:

Dr Loan Receivable $100

Cr Bank $100

As such, carrying amount of the asset is $100.

Tax treatment: When loan is given out, there is no tax consequence. When the loan is being repaid back to the entity, there is also no tax consequence.

In this case, the imaginary tax double entry in the imaginary tax financial statement is the same as the accounting double entry, i.e.

Dr Loan Receivable $100

Cr Bank $100

Tax base is also equal to $100.

As the CA and TB are the same, there will be no deferred tax.

Note: As mentioned previously in the definition of tax base for asset, "if those economic benefits will not be taxable, the tax base of the asset is equal to its carrying amount." As the repayment of loan has no tax implication (i.e.not taxable), the TB shall be equal to the CA.

That's all for this post! I believe you will have a lot to digest for now.

In my next post, I will discuss about how do we determine tax base for liability. Stay tuned!

No comments:

Post a Comment